Executive Summary

The Indian stock market has come full circle.

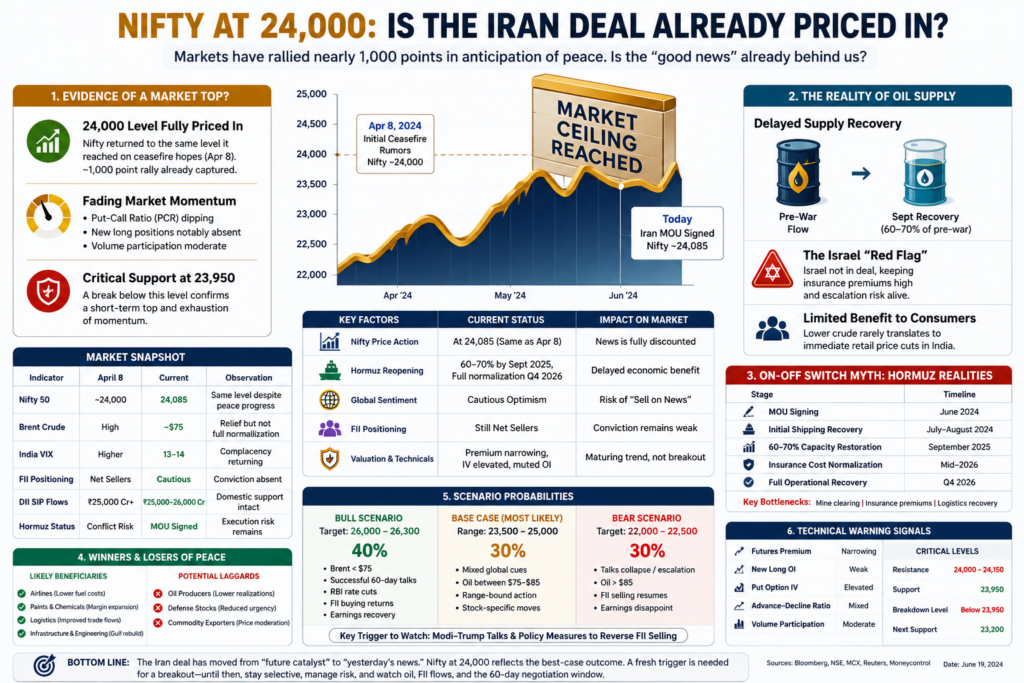

On April 8, when the first ceasefire headlines emerged, the Nifty 50 was trading near 24,000. Today, after the formal Iran-US framework agreement and the reopening roadmap for the Strait of Hormuz, the index is once again hovering around 24,000.

For long-term investors, this raises an important question:

If the market is already trading at the same level it reached on the first peace rumors, has the entire Iran deal already been priced in?

While falling crude oil prices, easing volatility, and strong domestic inflows remain supportive, institutional conviction is still missing. Foreign investors remain cautious, fresh long positions are limited, and several geopolitical risks continue to linger beneath the surface.

Key Market Metrics: Then vs Now

| Indicator | April 8 (Ceasefire Announcement) | Current Level | Strategic Observation |

|---|---|---|---|

| Nifty 50 | ~24,000 | ~24,085 | Market is trading at nearly the same level despite significant geopolitical progress. |

| Brent Crude Oil | Elevated | Trending Lower | Relief for India, but full supply normalization remains distant. |

| India VIX | Elevated | ~13–14 Range | Volatility has eased, indicating growing complacency. |

| FII Positioning | Net Sellers | Still Cautious | Foreign investors remain unconvinced. |

| DII Monthly SIP Flows | ₹25,000 Cr+ | ₹25,000–26,000 Cr | Domestic support remains strong. |

| Hormuz Status | Conflict Risk | MOU Signed | Execution risks still remain. |

What This Data Is Telling Investors

The market is effectively at the same level where it first reacted to peace expectations. This suggests that much of the positive news may already be reflected in prices.

The next phase of the rally will likely depend on:

- Sustained crude oil below $75

- Fresh FII buying

- Stronger corporate earnings

- RBI policy flexibility

- Successful implementation of the 60-day peace roadmap

1. The “Priced-In” Paradox

The Nifty has gained nearly 950 points in just a few sessions.

Historically, markets tend to move ahead of major events rather than after them. Institutional investors often buy expectations and sell confirmations.

This creates the classic:

“Buy the Rumor, Sell the News”

phenomenon.

The Iran framework agreement and Hormuz reopening roadmap are no longer future catalysts. They are now known information.

This explains why Nifty continues to struggle near the 24,000–24,100 zone despite positive headlines.

2. Why Oil Still Matters More Than Headlines

India imports nearly 85% of its crude oil requirement.

Every significant decline in oil prices directly impacts:

| Economic Variable | Impact |

|---|---|

| Inflation | Falls |

| Current Account Deficit | Improves |

| Fiscal Deficit | Improves |

| Corporate Margins | Expand |

| RBI Rate-Cut Potential | Increases |

The Critical Oil Threshold

| Brent Crude | Market Impact |

|---|---|

| Above $90 | Negative |

| $80–90 | Neutral |

| Below $75 | Bullish |

| Below $70 | Strongly Bullish |

The real bullish trigger for India is not peace itself.

It is sustained at crude below $75.

3. The Reality of Hormuz Reopening

Many investors assume that a signed agreement means immediate normalization.

History suggests otherwise.

Major Operational Challenges

| Challenge | Expected Impact |

|---|---|

| Mine Clearing Operations | Shipping Delays |

| Insurance Premiums | Higher Transport Costs |

| Tanker Availability | Supply Constraints |

| Port Congestion | Slower Normalization |

Expected Recovery Timeline

| Phase | Timeline |

|---|---|

| MOU Signed | Immediate |

| Partial Recovery | Q3 2026 |

| 60–70% Capacity | By September |

| Full Normalization | Late 2026 |

This means lower oil prices may arrive gradually rather than immediately.

4. The FII Problem Nobody Is Talking About

One of the biggest concerns remains foreign investor behavior.

Despite improved sentiment:

- Fresh long positions remain limited.

- Futures premiums are narrowing.

- Option hedging remains elevated.

- FIIs are still reluctant to chase higher valuations.

Market Participation Snapshot

| Participant | Current Behaviour |

|---|---|

| FIIs | Cautious |

| DIIs | Aggressive Buyers |

| Retail Investors | Bullish |

| Institutions | Selective |

Until FIIs begin accumulating rather than merely covering shorts, the rally remains vulnerable.

5. The Israel Factor Remains a Red Flag

Perhaps the largest risk remains geopolitical.

The framework agreement does not eliminate regional tensions.

Key concerns include:

- Verification disputes

- Regional military activity

- Israel’s independent position

- Potential escalation risks

Markets are currently pricing a successful outcome.

They are not pricing a major disruption.

This creates an asymmetric risk profile.

6. Technical View: Why 24,000 Matters

Key Levels to Watch

| Level | Importance |

|---|---|

| 24,200 | Breakout Zone |

| 24,000 | Psychological Barrier |

| 23,950 | Immediate Support |

| 23,750 | Strong Support |

| 22,000 | Major Downside Zone |

Technical Warning Signs

- Weak fresh Open Interest creation

- High Put Option IVs

- Narrow futures premium

- Limited institutional participation

These are characteristics of a relief rally rather than a strong trending bull market.

Scenario Analysis

Bull Case (35% Probability)

Conditions:

✅ Brent below $75

✅ Successful peace implementation

✅ Strong earnings recovery

✅ FII inflows return

Potential Target: 26,000+

Base Case (45% Probability)

Conditions:

✅ Mixed news flow

✅ Stable oil prices

✅ Moderate earnings growth

Expected Range: 23,500–25,000

Bear Case (20% Probability)

Conditions:

❌ Oil spike

❌ Geopolitical escalation

❌ Earnings disappointment

❌ Continued FII selling

Potential Target: 22,000–22,500

Investor Checklist

Before buying at current levels, ask yourself:

☐ Is crude oil sustainably below $75?

☐ Are FIIs buying aggressively?

☐ Is earnings growth improving?

☐ Is valuation still reasonable?

☐ Can I tolerate a 15–20% correction?

Final Verdict

The Iran framework agreement has undoubtedly reduced geopolitical uncertainty.

However, markets are forward-looking mechanisms.

The Nifty is currently trading at almost the same level where it stood when peace expectations first emerged. This strongly suggests that much of the optimism is already reflected in prices.

The next major move will not be determined by headlines.

It will be determined by:

- Oil prices

- Corporate earnings

- Foreign investor participation

- Global liquidity conditions

Bottom Line

The path to 26,000 requires strong earnings, lower oil prices, and renewed FII conviction. The path to 22,000 requires only one major macro shock.

Investors should focus less on peace headlines and more on the data that ultimately drives market returns.

Nifty Prediction 2026

Nifty Outlook 2026

Nifty Target 26000

Nifty Support and Resistance

Iran Deal Impact on the Indian Stock Market

Nifty Bull vs Bear Case

Nifty Analysis Today