Executive Summary

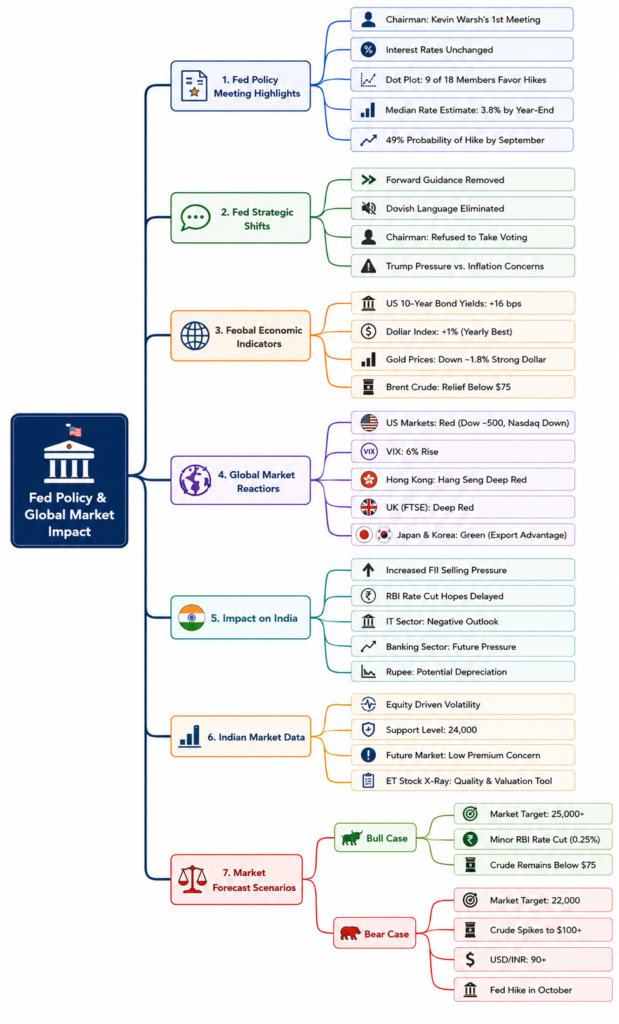

Global markets experienced a sharp reversal as investors digested the latest Federal Reserve policy signals. While the headline decision appeared unchanged, the underlying message was far more significant: interest rates may remain higher for longer than markets had anticipated.

The immediate reaction was swift:

- Dow Jones fell sharply

- Volatility surged

- Treasury yields jumped

- Gold weakened

- Emerging market sentiment deteriorated

For investors, the key question is no longer “When will rate cuts arrive?”

Instead, it is:

Can global markets continue higher if central banks keep liquidity tighter for longer?

Market Reaction Dashboard

| Asset Class | Market Reaction | Investor Interpretation |

|---|---|---|

| Dow Jones | Sharp Decline | Risk-Off Sentiment |

| Nasdaq | Weakness | Growth Stocks Under Pressure |

| VIX | +6% Surge | Fear Returning |

| US Dollar Index | Stronger | Dollar Demand Rising |

| Gold | Lower | Capital Moving Into Yield Assets |

| US Treasury Yields | Higher | Hawkish Rate Expectations |

Key Market Metrics

| Indicator | Previous Expectation | Current Outlook | Impact |

|---|---|---|---|

| Fed Rate Path | Rate Cuts Expected | Higher for Longer | Negative for Risk Assets |

| 2-Year Treasury Yield | Stable | Rising | Tightening Financial Conditions |

| US Dollar | Neutral | Strengthening | Pressure on Emerging Markets |

| Global Liquidity | Improving | Tightening | Risk Asset Headwind |

| Equity Valuations | Supported | Under Review | Volatility Risk |

The Dot Plot Shock

The Federal Reserve’s “Dot Plot” remains one of the most important tools for understanding policymakers’ future expectations.

Why Markets Reacted

| Factor | Market Interpretation |

|---|---|

| More Hawkish Expectations | Higher Rates Longer |

| Inflation Concerns Persist | Rate Cuts Delayed |

| Yield Curve Movement | Capital Repricing |

| Policy Uncertainty | Higher Volatility |

Markets were positioned for easier monetary policy.

Instead, they received a reminder that inflation remains a central concern.

The End of Easy Money

For over a decade, investors became accustomed to:

✅ Low interest rates

✅ Abundant liquidity

✅ Central bank support

Today the environment is different.

New Market Reality

| Old Environment | New Environment |

|---|---|

| Cheap Money | Expensive Capital |

| Aggressive Rate Cuts | Policy Patience |

| Valuation Expansion | Earnings Focus |

| Liquidity Driven | Fundamentals Driven |

This transition is forcing investors to reassess risk across all asset classes.

Global Winners and Losers

Potential Winners

| Region | Reason |

|---|---|

| Export-Oriented Economies | Benefit from Strong Dollar |

| High-Quality Value Stocks | Better Cash Flow Stability |

| Defensive Sectors | Lower Volatility |

| Strong Balance Sheet Companies | Higher Resilience |

Potential Losers

| Asset | Risk |

|---|---|

| High-Growth Unprofitable Companies | Funding Costs Rise |

| Highly Leveraged Firms | Debt Servicing Pressure |

| Emerging Markets | Capital Outflow Risk |

| Gold & Non-Yielding Assets | Competition from Bonds |

Why the Dollar Matters

The US Dollar remains the world’s reserve currency.

Dollar Impact Matrix

| Stronger Dollar Helps | Stronger Dollar Hurts |

|---|---|

| US Bonds | Emerging Markets |

| Export Economies | Commodity Importers |

| Dollar Savings | Gold Prices |

| US Capital Markets | High External Debt Nations |

A stronger dollar often creates tighter financial conditions globally.

India: The Yield Gap Challenge

India remains relatively strong due to:

- Robust domestic demand

- Consistent SIP inflows

- Stable banking system

- Structural economic growth

However, rising US yields create challenges.

India Market Dashboard

| Metric | Current Trend |

|---|---|

| FII Flows | Cautious |

| DII Flows | Strong |

| SIP Inflows | ₹25,000+ Cr Monthly |

| India VIX | Moderate |

| Rupee Stability | Important to Monitor |

| RBI Flexibility | Dependent on Inflation |

Sector Impact Analysis

Likely Beneficiaries

| Sector | Outlook |

|---|---|

| Banking | Stable |

| Capital Goods | Positive |

| Defense | Positive |

| Utilities | Defensive Strength |

| Large-Cap Quality Stocks | Preferred |

Potential Pressure Zones

| Sector | Reason |

|---|---|

| IT | Global Growth Sensitivity |

| Small Caps | Liquidity Risk |

| High-Debt Companies | Rising Funding Costs |

| Speculative Stocks | Valuation Compression |

Technical Risk Framework

Key Indicators Investors Should Monitor

| Indicator | Why It Matters |

|---|---|

| US 10-Year Yield | Global Cost of Capital |

| US Dollar Index (DXY) | Capital Flow Direction |

| India VIX | Market Risk Appetite |

| Brent Crude | Inflation Impact |

| FII Flows | Foreign Investor Confidence |

| Corporate Earnings | Market Sustainability |

Scenario Analysis

Bull Case (35%)

Conditions:

✅ Inflation falls faster

✅ Fed signals future easing

✅ Earnings surprise positively

✅ Global growth stabilizes

Potential Outcome

Risk assets recover and global equities move higher.

Base Case (45%)

Conditions:

✅ Rates remain elevated

✅ Growth moderates

✅ Inflation gradually improves

Potential Outcome

Range-bound markets with sector rotation.

Bear Case (20%)

Conditions:

❌ Inflation remains sticky

❌ More hawkish policy signals

❌ Global growth weakens

❌ Capital outflows increase

Potential Outcome

Higher volatility and broader market correction.

Risk Matrix

| Risk Factor | Severity |

|---|---|

| Higher Interest Rates | 🔴 High |

| Inflation Persistence | 🔴 High |

| Global Liquidity Tightening | 🔴 High |

| Dollar Strength | 🟠 Medium |

| Emerging Market Outflows | 🟠 Medium |

| Earnings Slowdown | 🟠 Medium |

Investor Checklist

Before making investment decisions, ask:

☐ Is my portfolio dependent on lower interest rates?

☐ Am I holding quality companies with strong cash flows?

☐ Can my portfolio withstand higher volatility?

☐ Am I diversified across sectors and asset classes?

☐ Am I investing based on fundamentals rather than headlines?

Final Verdict

The latest Federal Reserve message is not necessarily a market crash signal—but it is a warning that the era of easy money may be ending.

Markets now face a world where:

- Liquidity is less abundant

- Interest rates matter again

- Valuations face greater scrutiny

- Earnings quality becomes critical

Final Thought

Bull markets can survive higher interest rates, but speculative excess rarely can. Investors who focus on strong balance sheets, sustainable earnings, and disciplined risk management are likely to be better positioned for the next phase of the market cycle.

1.Fed Meeting Impact on Global Markets: Why Stocks Turned Red Overnight

2.Higher for Longer? What the Fed’s New Stance Means for Nifty, Gold & Global Markets

3.Fed Policy Shock 2026: Winners, Losers and Investment Strategy Explained

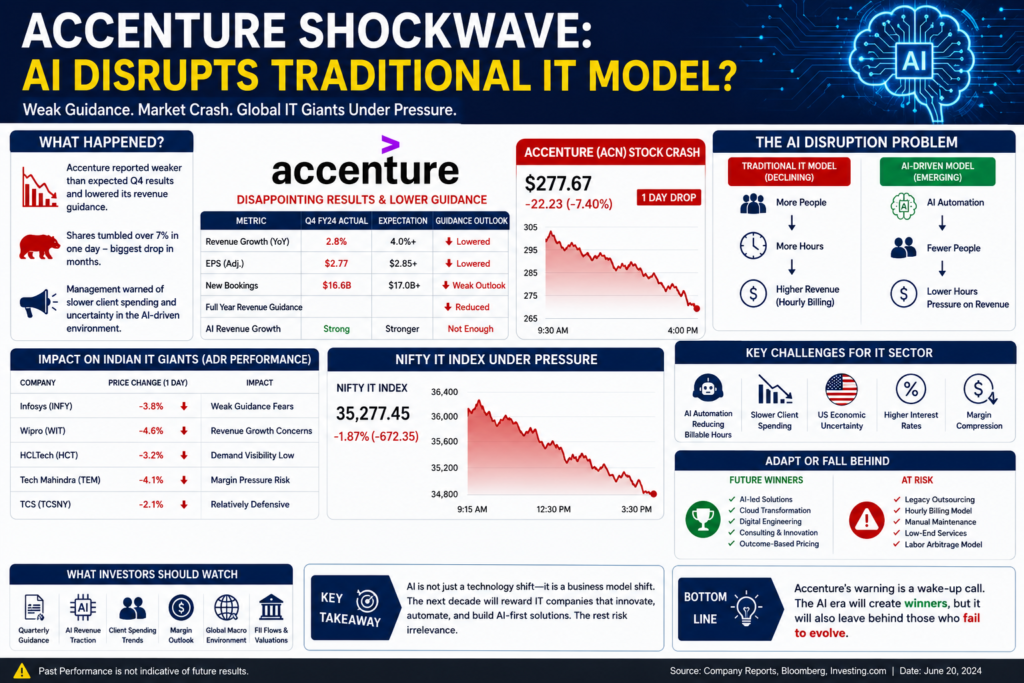

Accenture Shockwave: Is AI Disrupting the Global IT Industry Faster Than Expected?

Executive Summary

Global IT stocks came under severe pressure after Accenture, the world’s largest IT services company, released a disappointing quarterly earnings report and lowered its future revenue guidance.

The market reaction was swift and brutal:

- Accenture shares declined sharply.

- Indian IT ADRs weakened.

- The Nifty IT Index faced renewed selling pressure.

- Investors began questioning whether Artificial Intelligence is permanently disrupting the traditional IT outsourcing model.

The core concern is simple:

If AI can complete tasks faster and with fewer billable hours, what happens to the business model of companies that charge clients based on employee hours?

Why Accenture’s Results Matter

Accenture is often considered a global bellwether for the IT services industry.

When Accenture reports weaker growth, investors usually interpret it as a signal for the entire sector.

Quarterly Snapshot

| Metric | Previous Expectation | Current Reality |

|---|---|---|

| Revenue Growth | Strong Growth Expected | Slower Growth |

| Guidance | Stable Outlook | Lowered |

| AI Revenue | Growing | Not Enough to Offset Weakness |

| Client Spending | Expected Improvement | Remains Cautious |

| Market Reaction | Neutral | Sharp Sell-Off |

The biggest concern was not the quarterly numbers themselves.

It was management’s warning that clients continue to delay large technology spending decisions.

The AI Disruption Problem

For decades, IT service companies followed a simple model:

Traditional IT Model

Client Project

↓

More Engineers

↓

More Billable Hours

↓

Higher Revenue

Artificial Intelligence changes this equation.

AI Model

Client Project

↓

Automation & AI Tools

↓

Fewer Engineers Required

↓

Lower Billable Hours

↓

Pressure on Revenue

This creates a structural challenge for the entire industry.

Impact on Indian IT Companies

Indian IT companies remain heavily dependent on:

- North American clients

- Large outsourcing contracts

- Hourly billing models

- Long-term maintenance projects

When Accenture weakens, investors often assume similar pressures will affect Indian firms.

Immediate Market Impact

| Company | Market Sentiment |

|---|---|

| Infosys | Negative |

| Wipro | Negative |

| HCLTech | Cautious |

| Tech Mahindra | Negative |

| TCS | Relatively Defensive |

Why Nifty IT Is Under Pressure

Several headwinds are hitting the sector simultaneously.

Key Challenges

| Challenge | Impact |

|---|---|

| AI Automation | Revenue Pressure |

| Slower Client Spending | Lower Growth |

| US Economic Uncertainty | Delayed Projects |

| Higher Interest Rates | Lower Tech Budgets |

| Margin Compression | Profitability Risk |

The market is increasingly asking:

Can traditional IT outsourcing grow at historical rates in an AI-driven world?

Winners vs Losers in the AI Era

Potential Winners

| Category | Examples |

|---|---|

| AI Infrastructure | NVIDIA |

| Cloud Platforms | AWS, Azure, Google Cloud |

| AI Software Leaders | OpenAI Ecosystem |

| Semiconductor Firms | TSMC, Broadcom |

Potential Losers

| Category | Risk |

|---|---|

| Hourly Billing Companies | High |

| Legacy Maintenance Services | High |

| Low-End Outsourcing | Very High |

| Manual Testing Businesses | High |

What Investors Should Watch

Key Indicators

| Indicator | Why It Matters |

|---|---|

| Accenture Guidance | Global IT Demand |

| US Corporate Spending | Client Budgets |

| AI Revenue Growth | Future Business Model |

| Nifty IT Performance | Sector Sentiment |

| FII Activity | Institutional Confidence |

Bull Case for IT

Conditions Required

✅ AI services grow faster than traditional services

✅ Clients increase digital transformation spending

✅ US economy avoids recession

✅ Indian firms successfully monetize AI solutions

Potential Outcome

- Earnings recovery

- Improved valuations

- Nifty IT leadership returns

Bear Case for IT

Risks

❌ AI reduces billable hours permanently

❌ Clients spend less on outsourcing

❌ Revenue growth continues slowing

❌ Margins compress

Potential Outcome

- Lower earnings growth

- Valuation correction

- Continued underperformance

Investor Strategy

Short-Term (0–12 Months)

- Focus on quality IT leaders.

- Avoid highly leveraged companies.

- Watch earnings guidance closely.

Long-Term (3–10 Years)

The IT sector is unlikely to disappear.

However, the winners will be companies that successfully transition from:

“Selling employee hours” → “Selling AI-powered solutions.”

Final Verdict

Accenture’s warning is more than a single quarterly disappointment.

It represents a broader industry challenge.

Artificial Intelligence is reshaping how technology services are delivered, priced, and consumed.

The next decade will likely create two groups:

- Companies that adapt to AI.

- Companies that get disrupted by AI.

For investors, the question is no longer whether AI will impact IT services.

The question is:

Which companies will benefit from AI—and which companies will be replaced by it?