RBI’s Emergency Forex Swap: Banking Rally or Warning Signal?

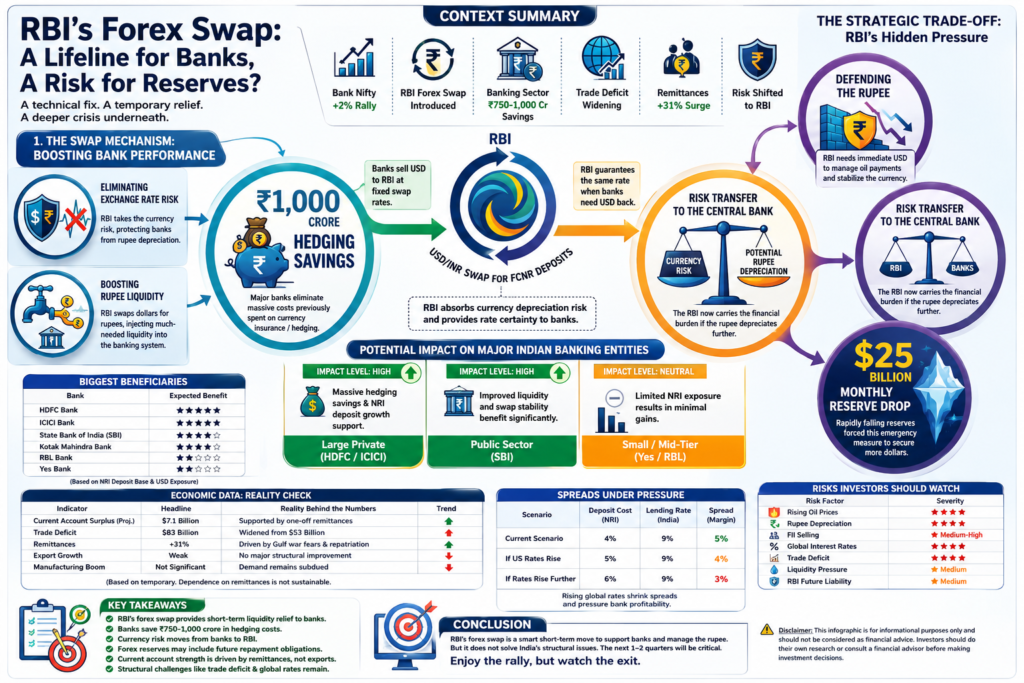

Indian banking stocks recently witnessed a sharp rally, with Bank Nifty gaining over 2% despite weak global cues and persistent FII selling. At first glance, investors celebrated the move as a sign of strength. However, beneath this optimism lies a much bigger story.

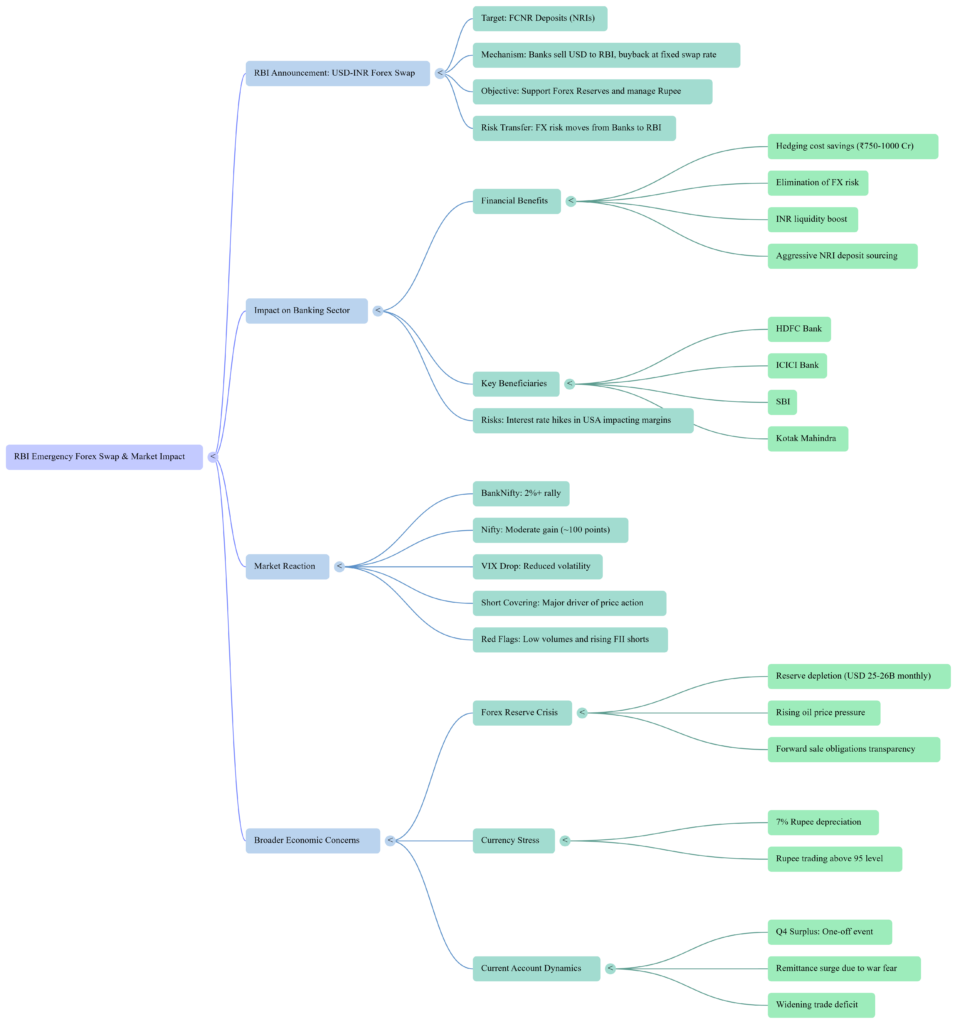

The Reserve Bank of India (RBI) introduced a special USD-INR Forex Swap facility for FCNR deposits, a technical policy that appears designed to solve an urgent liquidity and foreign exchange problem rather than stimulate long-term economic growth.

The key question investors should ask is:

Is this a genuine banking recovery, or merely a temporary rescue operation?

Quick Highlights

| Indicator | Current Situation | Impact |

|---|---|---|

| Bank Nifty | +2% Rally | Positive Short-Term |

| RBI Forex Swap | Introduced | Liquidity Support |

| Banking Sector Benefit | ₹750-1000 Crore Savings | Bullish |

| Trade Deficit | Increased | Negative |

| Remittances | +31% | Temporary Support |

| Forex Risk | Shifted to RBI | Hidden Liability |

| Long-Term Outlook | Uncertain | Cautious |

Understanding the RBI Forex Swap

Normally, when NRIs deposit dollars into Indian banks through FCNR accounts, banks convert those dollars into rupees for lending purposes.

The problem arises when:

- Rupee depreciates

- Banks must return dollars later

- The dollar becomes expensive

- Banks suffer forex losses

Earlier, banks had to purchase expensive hedging contracts to protect themselves.

Now the RBI is effectively saying:

“Deposit your dollars with us today, and we’ll guarantee the exchange rate when repayment becomes due.”

This significantly reduces currency risk for banks.

How the Risk Gets Transferred

Earlier System

| Process | Risk Holder |

| NRI deposits dollars | Bank |

| Bank converts into INR | Bank |

| Rupee depreciates | Bank bears loss |

| Dollar repayment | Bank pays higher cost |

New RBI Swap System

| Process | Risk Holder |

| NRI deposits dollars | Bank |

| RBI accepts dollars | RBI |

| Exchange rate guaranteed | RBI |

| Currency fluctuation | RBI bears risk |

Result:

Banks become safer while the RBI absorbs forex uncertainty.

Biggest Beneficiaries

| Bank | Expected Benefit |

| HDFC Bank | High |

| ICICI Bank | High |

| SBI | High |

| Kotak Mahindra Bank | High |

| RBL Bank | Limited |

| Yes Bank | Limited |

Large banks with significant NRI deposit bases stand to gain the most.

Estimated Financial Savings

| Factor | Estimated Value |

| Hedging Cost Saved | ₹750-1000 Crore |

| Immediate Liquidity | Positive |

| Banking Profitability | Improved |

| Market Sentiment | Bullish |

This explains why banking stocks rallied almost immediately after the announcement.

Why Did RBI Introduce This Facility?

Several structural challenges exist:

- Tight liquidity

- Persistent FII selling

- Rising oil import bill

- Pressure on the Rupee

- Limited room for interest rate adjustments

Instead of cutting rates aggressively, the RBI has injected liquidity through forex swaps.

Think of it as providing oxygen to the banking system without changing policy rates.

The Forex Reserve Mirage

Many investors focus only on rising forex reserves.

However, there’s another side.

RBI Gets

- Immediate USD inflow

- Stronger reserve numbers

- Better ability to defend INR

RBI Gives

- Future obligation to return dollars

- Exchange rate guarantee

- Currency risk on its own balance sheet

Therefore, today’s reserve growth may also represent tomorrow’s liability.

Current Account Surplus: Reality vs Headlines

Many reports highlighted a projected $7.1 Billion Current Account Surplus.

But the detailed picture looks different.

| Headline | Reality |

| Current Account Surplus | $7.1 Billion |

| Trade Deficit | Increased to $83 Billion |

| Export Growth | Weak |

| Manufacturing Boom | Not Significant |

| Remittance Growth | +31% |

The surplus appears heavily supported by remittances rather than structural export strength.

Why Remittances Increased

Possible contributing factors include:

- Gulf geopolitical uncertainty

- Capital repatriation

- Family transfers

- Risk management by overseas workers

If these flows normalize, the underlying trade imbalance could become more visible.

Biggest Long-Term Risk

Banks earn profits through spreads.

Example:

| Item | Rate |

| FCNR Deposit Cost | 4% |

| Lending Rate | 9% |

| Profit Spread | 5% |

If US interest rates rise:

| Item | New Rate |

| Deposit Cost | 5% |

| Lending Rate | 9% |

| Spread | 4% |

Lower spreads reduce profitability.

RBI’s forex swap protects against currency volatility—but not against changes in the global interest rate cycle.

Risks Investors Should Watch

| Risk | Severity |

| Rising Oil Prices | High |

| Rupee Depreciation | High |

| FII Selling | Medium-High |

| Global Interest Rates | High |

| Trade Deficit | High |

| Liquidity Pressure | Medium |

| RBI Future Liability | Medium |

Key Takeaways

✅ Banking rally is supported by RBI liquidity measures.

✅ Banks save substantial hedging costs.

✅ Currency risk shifts from banks to RBI.

✅ Rising forex reserves may include future obligations.

✅ Current account surplus relies heavily on remittances.

✅ Structural trade deficit remains a concern.

✅ Investors should distinguish between short-term sentiment and long-term fundamentals.

Conclusion

The RBI’s emergency forex swap is an intelligent short-term liquidity tool, but it does not eliminate India’s structural economic challenges. It reduces currency risk for banks and supports market confidence, yet issues such as trade deficits, global rate pressures, and dependence on temporary capital flows remain.

For long-term investors, the banking rally may present opportunities, but it should be evaluated alongside the broader macroeconomic picture rather than viewed as proof that underlying risks have disappeared.

Frequently Asked Questions (FAQ)

What is the RBI Forex Swap?

A mechanism where RBI exchanges dollars and rupees with banks while providing exchange-rate protection.

Why did banking stocks rally?

Because banks may save significant hedging costs and receive improved liquidity support.

Who benefits the most?

Large banks with substantial FCNR/NRI deposit bases.

Is this bullish for the economy?

It is supportive in the short term, but long-term economic strength depends on trade, investment, productivity, and sustainable capital flows.

Should investors worry?

Investors should monitor macroeconomic indicators such as forex reserves, trade deficit, oil prices, and global interest rates instead of relying solely on market rallies.