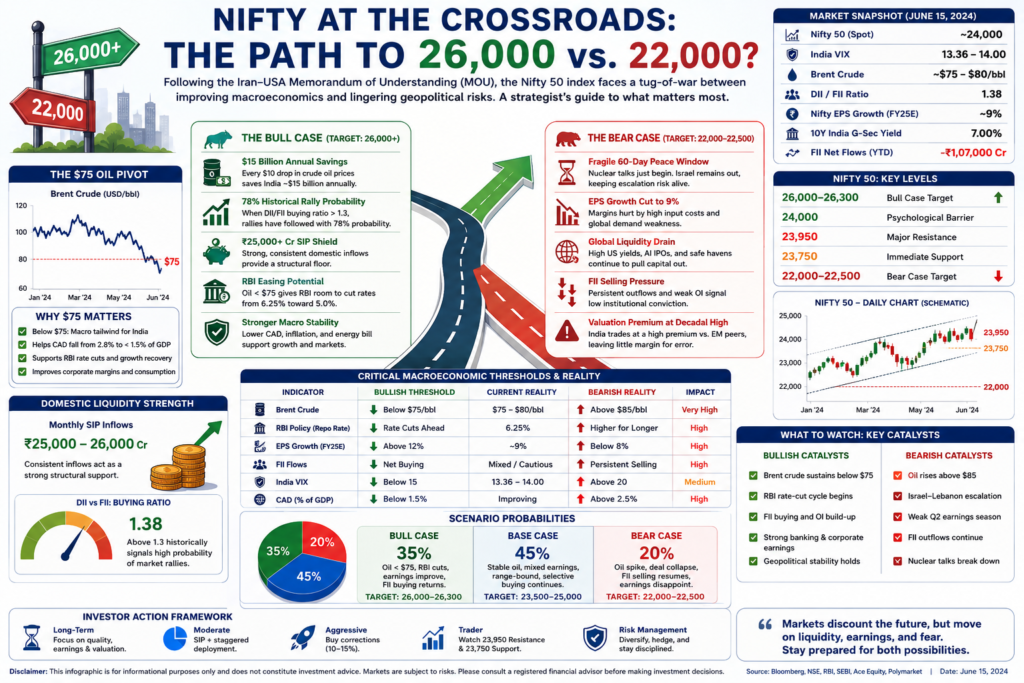

Executive Summary

The Indian market has staged an impressive recovery following the June 15 geopolitical framework agreement involving the United States and Iran. The Nifty rebounded nearly 800 points and once again approached the psychologically important 24,000 mark.

Yet beneath the headlines lies a critical question:

Is this the beginning of a new bull phase toward 26,000+, or merely a relief rally inside a broader consolidation cycle?

While falling crude oil prices and resilient domestic inflows provide support, several structural challenges remain:

- Weak earnings growth

- Elevated valuations

- Continued FII caution

- Global liquidity competition

- Unresolved geopolitical risks

The battle between 26,000 and 22,000 may ultimately be decided not by headlines—but by oil, earnings, and liquidity.

Market Snapshot

| Indicator | Current Reading | Implication |

|---|---|---|

| Nifty 50 | Near 24,000 | Testing major resistance |

| India VIX | 13–14 Range | Calm but vulnerable |

| Brent Crude | Near $75-$80 | Key macro variable |

| FII Positioning | Cautious | Limited conviction |

| DII Flows | Strong | Market support |

| Nifty EPS Growth | Reduced to ~9% | Earnings slowdown |

Why Markets Rallied

The market reacted positively to:

✅ Reduced geopolitical uncertainty

✅ Falling oil prices

✅ Short covering by traders

✅ Strong domestic inflows

✅ Expectations of future RBI easing

However, professional investors are asking:

Where is the fresh long-term institutional buying?

The Oil Equation: India’s Most Important Macro Variable

For India, crude oil remains the single most important external variable.

Impact of Oil Prices

| Brent Price | Economic Impact |

|---|---|

| Above $90 | Inflation Risk |

| $80-$90 | Manageable Pressure |

| Below $75 | Bullish for Growth |

| Below $70 | Strong Macro Tailwind |

Why $75 Oil Matters

A sustained move below $75 creates multiple benefits.

Macro Impact

| Factor | Potential Benefit |

|---|---|

| Current Account Deficit | Improves |

| Inflation | Falls |

| Fiscal Position | Strengthens |

| Corporate Margins | Expand |

| RBI Policy Flexibility | Increases |

Historically, Indian equities tend to outperform when oil remains below major stress levels.

Domestic Liquidity: India’s Permanent Bid

India’s SIP ecosystem has transformed market dynamics.

Monthly Domestic Flow

| Source | Approximate Flow |

|---|---|

| SIP Contributions | ₹25,000–26,000 Crore |

| Mutual Fund Inflows | Strong |

| Retail Participation | Record Levels |

This domestic liquidity has absorbed significant foreign selling pressure.

DII vs FII Battle

| Metric | Observation |

|---|---|

| FII Selling | Elevated |

| DII Buying | Aggressive |

| DII/FII Ratio | ~1.38 |

| Historical Signal | Generally Positive |

Historical Observation

When DII buying significantly outweighs FII selling, market corrections often become shallower.

The Valuation Problem

Despite strong liquidity support, valuations remain elevated.

Relative Valuation Comparison

| Market | Relative PE Premium |

|---|---|

| India | High |

| Emerging Markets | Lower |

| Developed Markets | Mixed |

India currently trades at one of the highest valuation premiums among major emerging markets.

The 60-Day Trap

Many investors are treating the geopolitical framework as a permanent resolution.

The reality is more complex.

Current Framework

Framework Agreement

↓

60-Day Negotiation Window

↓

Verification Process

↓

Implementation

↓

Permanent Settlement (If Successful)

Major Risks Still Unresolved

| Risk | Status |

|---|---|

| Nuclear Verification | Pending |

| Regional Security Issues | Unresolved |

| Shipping Insurance Costs | Elevated |

| Supply Chain Normalization | Gradual |

| Energy Stability | Not Guaranteed |

The agreement may reduce risk, but it does not eliminate it.

Global Liquidity Challenge

India is no longer competing only with other emerging markets.

It is competing against:

- US Treasuries

- AI Infrastructure Spending

- Large Technology IPOs

- Global Private Capital

Where Global Money Is Going

| Destination | Capital Attraction |

|---|---|

| US Treasuries | High |

| AI Infrastructure | Very High |

| Mega IPOs | High |

| Emerging Markets | Moderate |

This creates a headwind for sustained FII inflows.

Earnings Reality Check

Corporate earnings remain the biggest concern.

EPS Growth Expectations

| Period | Growth Estimate |

|---|---|

| Earlier Forecast | ~15% |

| Current Estimate | ~9% |

Lower earnings growth naturally reduces valuation support.

Sector Outlook

Potential Winners

| Sector | Outlook |

|---|---|

| Banking | Positive if rates fall |

| Realty | Positive |

| Auto | Positive |

| Aviation | Positive |

| Consumer Discretionary | Positive |

Sectors Under Pressure

| Sector | Challenge |

|---|---|

| FMCG | Input Cost Inflation |

| Cement | Margin Pressure |

| Paints | Raw Material Costs |

| Industrials | Energy Costs |

| Export-Oriented Businesses | Global Weakness |

Technical Framework

Key Nifty Levels

| Level | Importance |

|---|---|

| 24,000 | Psychological Barrier |

| 23,950 | Immediate Resistance |

| 23,750 | Near-Term Support |

| 22,000 | Major Downside Support |

Scenario Analysis

Bull Case

Probability: 35%

Conditions:

- Oil remains below $75

- Geopolitical stability continues

- RBI becomes accommodative

- Earnings improve

Potential Target:

26,000+

Base Case

Probability: 45%

Conditions:

- Mixed news flow

- Stable oil

- Moderate earnings

Potential Outcome:

Range-bound between 23,500–25,000

Bear Case

Probability: 20%

Conditions:

- Geopolitical escalation

- Oil spike

- Earnings disappointment

- Continued FII outflows

Potential Target:

22,000–22,500

Risk Matrix

| Risk Factor | Severity |

|---|---|

| Oil Shock | 🔴 High |

| Geopolitical Escalation | 🔴 High |

| FII Selling | 🟠 Medium |

| Valuation Compression | 🟠 Medium |

| Earnings Slowdown | 🟠 Medium |

| Global Liquidity Tightening | 🔴 High |

What Smart Investors Should Monitor

Daily

✅ Brent Crude

✅ India VIX

✅ FII Flows

✅ USD/INR

✅ Global Bond Yields

Weekly

✅ Corporate Earnings Updates

✅ RBI Commentary

✅ Mutual Fund Flows

✅ Market Breadth

Investor Checklist

Before chasing the rally, ask:

☐ Is this move supported by earnings?

☐ Is fresh institutional money entering?

☐ Is oil sustainably below $75?

☐ Am I buying quality businesses?

☐ Can I hold through a 15–20% correction?

Final Verdict

The post-deal rally has improved sentiment, but sentiment alone does not create sustainable bull markets.

The market currently sits between two powerful forces:

Bullish Forces

- Falling crude oil

- Strong SIP flows

- Domestic liquidity

- Potential rate cuts

Bearish Forces

- Slowing earnings

- High valuations

- Global liquidity competition

- Geopolitical uncertainty

Final Thought

The path to 26,000 requires earnings growth, stable oil prices, and renewed institutional participation. The path to 22,000 requires only one major macro shock. In the current environment, investors should focus less on headlines and more on liquidity, earnings, and valuation discipline.